The Rising Legal Risk of NBFC Loan Default

In recent years, loan defaults with NBFCs (Non-Banking Financial Companies) have sharply risen in India, causing both borrowers and lenders to enter into complex legal disputes. According to an RBI report published in 2023, NBFCs now account for over 30% of the total retail lending market in India. With such a massive footprint, NBFC loan default legal action is becoming a real concern for thousands of borrowers.

If you're someone who has taken a loan from an NBFC and missed one or more EMIs, you may be wondering: Can NBFCs really take legal action against me? What are my rights? And how can I deal with NBFC harassment or legal threats? This blog covers all the answers you need, with legal remedies tailored to Indian laws and regulations.

What Are NBFCs and How Do They Operate in India?

Understanding NBFCs vs Traditional Banks

NBFCs (Non-Banking Financial Companies) are financial institutions registered under the Companies Act, 2013 and regulated by the Reserve Bank of India (RBI).

Unlike banks, NBFCs do not hold a banking license. They cannot accept demand deposits (like savings/current accounts) but can lend money and offer financial services.

Common Types of NBFCs in India:

NBFC-MFIs (Microfinance Institutions)

NBFC-HFCs (Housing Finance Companies)

NBFC-IFCs (Infrastructure Finance Companies)

NBFC-Factors (Specialized in Bill Discounting)

NBFCs have become popular for quick loan disbursals, fewer formalities, and easier access to credit. However, this comes with a price: higher interest rates and strict recovery tactics.

Can NBFCs Take Legal Action for Loan Default?

Yes, NBFCs can legally take action against borrowers who default on their loans, especially if the default continues beyond a reasonable time and after multiple reminders.

Legal Basis for NBFC Action:

Indian Contract Act, 1872: Once you sign a loan agreement, you’re legally bound to repay.

SARFAESI Act, 2002: While mostly used by banks, large NBFCs registered with RBI as secured lenders can also invoke SARFAESI.

Civil Lawsuits: NBFCs can file civil suits for recovery under the Code of Civil Procedure (CPC).

Criminal Proceedings: Only in case of cheque bounce (Section 138 of the Negotiable Instruments Act) or fraud (Sections 420 IPC, etc.)

Primary Keyword Usage: NBFC loan default legal action is backed by both civil and occasionally criminal laws.

NBFC Harassment: What Is It and How to Deal With It

Many borrowers complain of NBFC harassment in the form of threatening calls, home visits, or contacting family and employers.

What Constitutes Harassment?

Abusive language or threats by recovery agents

Visiting your home or office repeatedly

Public humiliation

Calling your employer or family

Legal Remedies Against NBFC Harassment:

RBI Guidelines on Fair Practices Code: NBFCs must follow ethical collection practices. RBI Fair Practices Code

Police Complaint: You can file a complaint under IPC Sections 503 (criminal intimidation), 504 (insult), and 506 (threat).

Complaint to RBI Ombudsman: Lodge an online complaint through https://cms.rbi.org.in

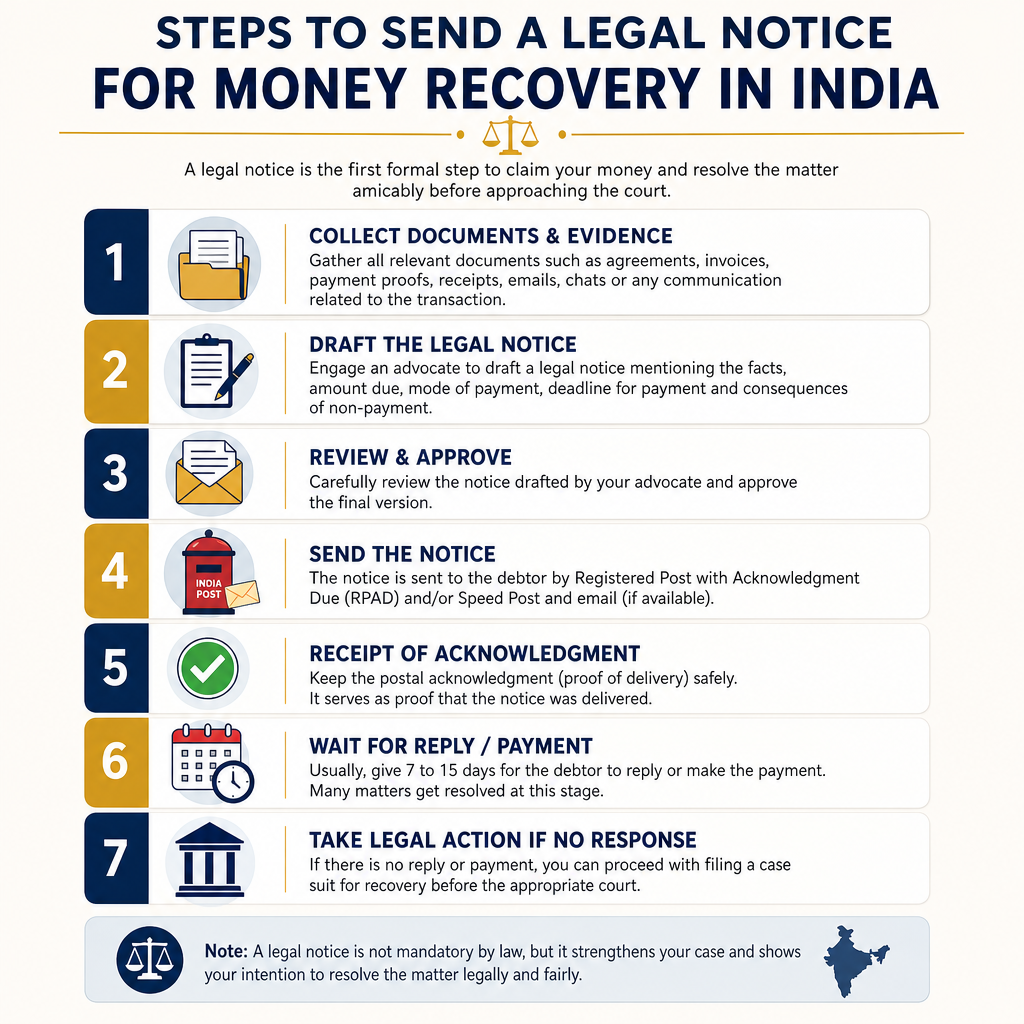

Send Legal Notice: A legal notice from a lawyer often curbs illegal recovery methods.

Internal Link: Learn how to file a complaint against recovery agents in India

Legal Remedies Available to Borrowers

If you’re facing NBFC loan default legal action, you still have options before the matter escalates.

1. Loan Restructuring:

2. One-Time Settlement (OTS):

3. Insolvency Under IBC (Individuals):

Under the Insolvency and Bankruptcy Code (IBC), individuals can file for bankruptcy protection

Best for cases where liabilities far exceed income

4. Legal Representation:

Internal Link: Explore our Loan Settlement Services

What Happens if You Ignore NBFC Loan Default?

Ignoring NBFC notices can lead to:

Civil suits for recovery

Negative CIBIL and credit bureau reporting

Warrants in cheque bounce cases

Possession of secured assets (in SARFAESI cases)

Attachment of salary or property (post decree)

Always respond to notices. Consulting a lawyer can help in avoiding irreversible damage.

Internal Link: Get expert help for Legal Notices

Rights of Borrowers in Case of NBFC Loan Default

1. Right to Fair Treatment

2. Right to Notice

3. Right to Settle

4. Right to Be Heard

Secondary Keyword Usage: NBFC harassment is prohibited and can be legally challenged under RBI and Indian laws.

How Courts in India View NBFC Loan Defaults

Indian courts recognize the borrower’s legal obligation to repay loans but also protect them from illegal recovery methods.

Notable Judgments:

ICICI Bank Ltd v. Shanti Devi Sharma (Delhi HC): Ruled that recovery agents cannot use coercive methods

Manager, ICICI Bank v. Prakash Kaur (SC): Strong remarks against banks and NBFCs using muscle power

Borrowers have rights and must exercise them through proper legal channels.

Tips to Avoid NBFC Loan Default Legal Action

Keep track of EMI dates

Communicate financial hardship in writing

Avoid cheque payments if funds are insufficient

Maintain copies of all communications with NBFC

Take legal advice early

Internal Link: Book a Legal Consultation with AMA Legal Solutions

Know Your Rights and Act Wisely

Yes, NBFCs can take legal action for loan default in India, but the law also protects borrowers from unfair practices. You are not alone—many individuals across India face similar issues. What matters is how quickly and smartly you respond.

At AMA Legal Solutions, we help borrowers deal with NBFC loan default legal action, settlement negotiation, and recovery harassment. Our experienced legal team in Gurgaon ensures your rights are upheld and your legal risks minimized.

Contact us today to safeguard your financial future.

Statistical Fact: As per a 2024 RBI bulletin, NBFC retail loan delinquencies have crossed 4.6%, the highest in a decade.