In India, the adoption of credit cards has been growing rapidly. As of 2024, the Reserve Bank of India (RBI) reports over 100 million active credit cards, with millions of users facing challenges in managing timely repayments (RBI Annual Report). While credit cards provide convenience and access to instant credit, they often come with high interest rates, penalties, and fees. Missing payments can quickly lead to unmanageable debt.

For cardholders struggling with dues, One Card Settlement is a practical solution. It allows borrowers to negotiate a reduced settlement amount with their bank, closing their credit card account legally and efficiently.

📊 Stat: According to TransUnion CIBIL, nearly 11% of credit card users default on payments for more than 90 days, and around 7 out of 10 of these users explore settlement options.

At AMA Legal Solutions, Sector 57 Gurugram, we help clients navigate One Card Settlement professionally, ensuring compliance, proper documentation, and protection from unnecessary harassment.

This blog will cover the process, benefits, risks, alternatives, and impact on your credit score, with expert insights and step-by-step guidance.

What is One Card Settlement?

One Card Settlement is an agreement between a cardholder and their bank in which the bank accepts a reduced lump-sum payment as full settlement of outstanding dues. Unlike restructuring or full repayment, this option allows borrowers to close their account at a negotiated amount, often saving significant money.

This solution is usually offered when:

Payments are overdue for 90+ days

Borrowers face financial hardship (job loss, medical expenses, business losses)

The account is classified as a Non-Performing Asset (NPA)

For example, a cardholder with ₹1,50,000 outstanding may settle the debt for ₹90,000. The account is then reported as “Settled” in credit bureau records.

📊 Stat: Banks recover 40–70% of overdue balances through settlements (RBI Report).

💡 Infographic Idea: Comparison chart of Regular Payment, Restructuring, and One Card Settlement.

🔗 Related Read: Loan Settlement and Its Impact on Credit Score

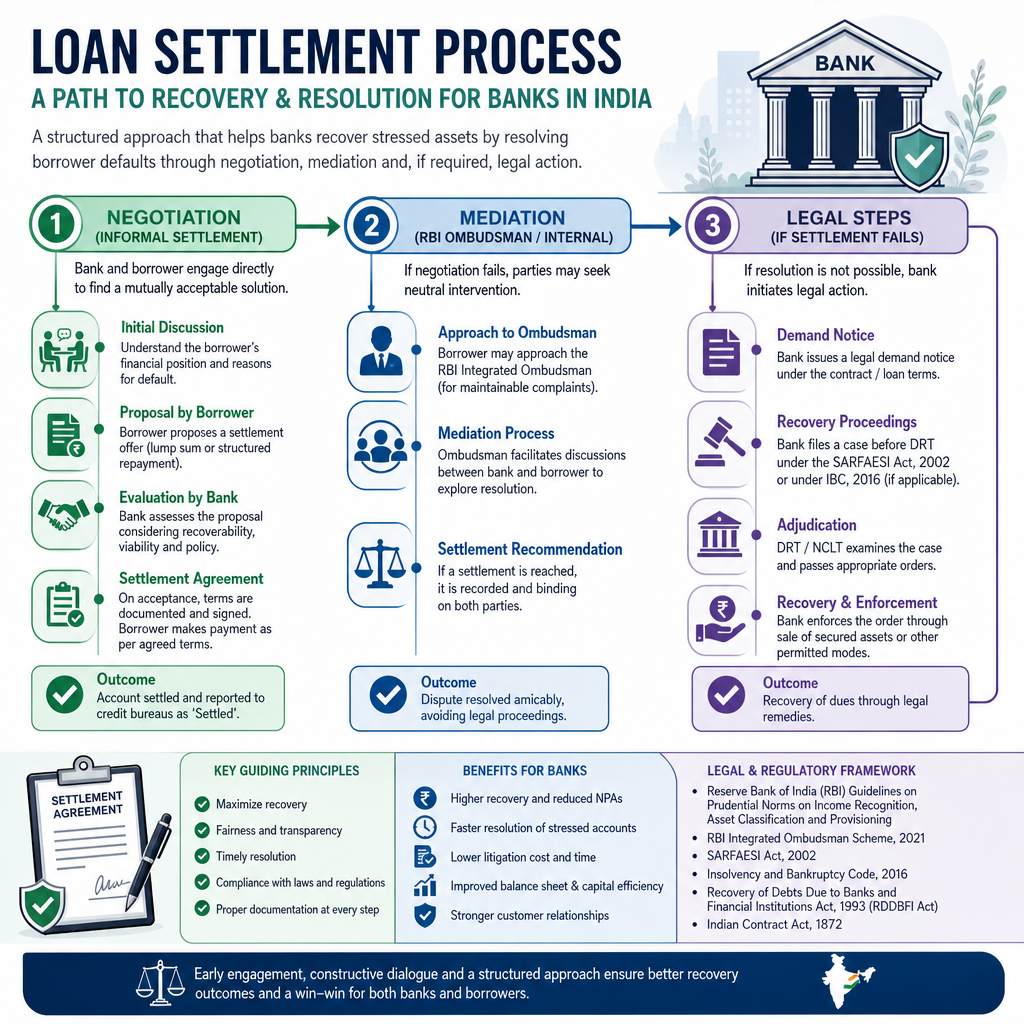

The One Card Settlement Process

The One Card Settlement process is methodical, requiring careful planning and legal guidance.

Debt Assessment – Calculate total dues, including principal, interest, fees, and penalties.

Settlement Request – Approach the bank’s collections team directly or via a legal service provider.

Negotiation – Banks usually settle for 30–70% of total dues, depending on account status.

Documentation – Obtain a formal settlement letter confirming the agreed amount.

Payment – Make the payment in a lump sum or structured installments.

No Dues Certificate (NDC) – Ensure proof of full settlement is issued.

At AMA Legal Solutions, we handle the entire process, including negotiation and legal documentation, ensuring your settlement is smooth and legally valid.

Advantages and Disadvantages of One Card Settlement

✅ Advantages

Immediate Relief – Stops collection calls and harassment.

Reduced Payment – Pay a fraction of the outstanding balance.

Avoid Legal Action – Prevents escalation to the Debt Recovery Tribunal.

Faster Resolution – Accounts are closed much faster than through regular repayment.

Peace of Mind – Reduces financial stress and uncertainty.

❌ Disadvantages

Impact on Credit Score – “Settled” accounts lower your credit rating.

Future Loan Restrictions – May reduce the likelihood of approvals for home, personal, or business loans.

Temporary Relief – Does not address underlying spending habits.

Documentation Risk – Poor documentation can lead to disputes with the bank.

Potential Tax Implications – Settled debt may be considered taxable income in some cases.

📊 Stat: Accounts marked as “Settled” reduce loan approval chances by 60% (TransUnion CIBIL).

Step-by-Step Guide to One Card Settlement

Evaluate Your Financial Position – Understand how much you can afford to pay.

Approach the Bank – Contact the bank’s collections team or use a legal intermediary.

Engage Legal Experts – Professionals like AMA Legal Solutions help negotiate better settlements.

Negotiate Settlement Terms – Discuss percentages and payment timelines (usually 30–70% of dues).

Document the Agreement – Ensure the agreement is in writing and legally binding.

Make Payment & Obtain NDC – Complete the settlement and keep the No Dues Certificate for future proof.

How One Card Settlement Impacts Your Credit Score

Reported as “Settled”, not “Closed”

CIBIL score may drop 40–100 points

Settled status remains for 7 years

Future lenders may view settlements negatively

📊 Stat: Borrowers with settlements are 50% less likely to get new loans within three years (CIBIL).

Important Considerations Before Opting for One Card Settlement

Explore if restructuring EMIs is possible.

Consider the impact on long-term financial goals.

Ensure fair negotiation via AMA Legal Solutions.

Verify documentation for legal compliance.

🔗 Internal Resource: Arbitration Process in India for Loan Settlement

Alternatives to One Card Settlement

Restructuring EMIs – Smaller, manageable monthly payments.

Balance Transfer – Transfer dues to a lower-interest card.

Debt Consolidation Loan – Merge multiple debts into one EMI.

Legal Mediation – Services like AMA Legal Solutions negotiate settlements.

Bank Hardship Programs – Temporary relief for eligible borrowers.

One Card Settlement provides short-term relief, stopping harassment and reducing dues. However, it negatively impacts your credit score and future loan eligibility.

📊 Stat: RBI data shows 12% of unsecured loan customers in India opt for settlements annually (RBI Circular).

At AMA Legal Solutions, Sector 57 Gurugram, we help clients negotiate settlements, ensure compliance, and obtain legally valid closure.