Understanding CIBIL Score and Its Importance

The CIBIL score is a three-digit numeric summary of your credit history, ranging from 300 to 900, with a higher score indicating better creditworthiness. It is generated by the Credit Information Bureau (India) Limited (CIBIL) and is used by lenders to evaluate your credit behavior before approving loans or credit cards.

Having a good CIBIL score is crucial as it impacts your ability to secure loans, the interest rates offered, and even your eligibility for certain jobs or rental agreements. A good CIBIL score generally falls between 750 and 900. Lenders consider individuals within this range as low-risk borrowers. Conversely, a score between 300 and 600 is considered poor, making it challenging to get loan approvals.

Understanding your CIBIL score's importance is the first step toward managing your financial health and ensuring you have access to credit when needed.

Maintaining a high CIBIL score not only helps in securing loans but also ensures that you get favorable interest rates and terms. This can save you a significant amount of money over the life of a loan. Additionally, a strong CIBIL score can provide peace of mind, knowing that your financial behavior is in good standing and that you have the flexibility to manage any financial needs that arise.

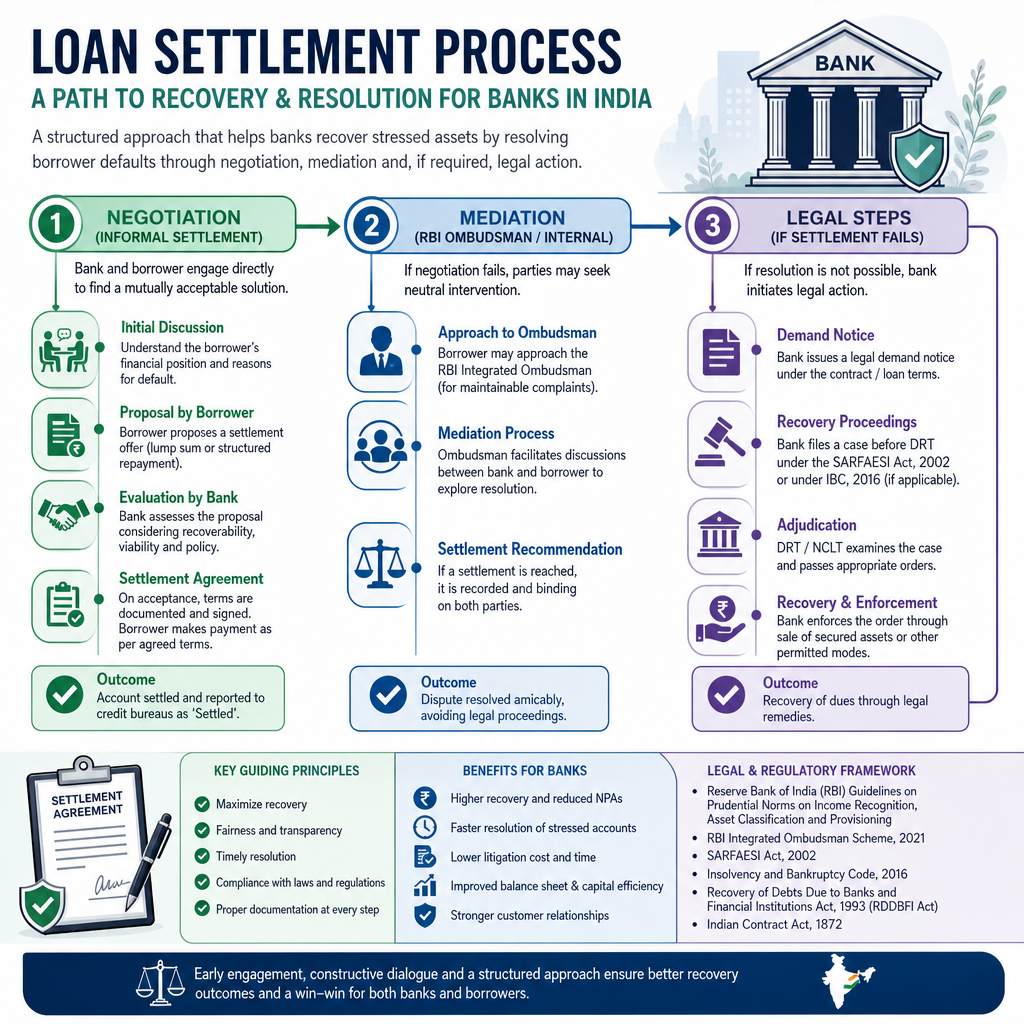

What Happens to Your CIBIL Score After Loan Settlement?

Loan settlement occurs when a borrower and lender agree to resolve an outstanding debt for less than the total amount owed. While this may seem like a favorable solution when you're financially strained, it has a significant impact on your CIBIL score. Loan settlements are reported to credit bureaus and noted in your credit report, leading to a considerable drop in your score.

When a loan is settled, it indicates to future lenders that you were unable to repay your debt in full. This raises red flags and signals a higher risk, making lenders wary of extending new credit to you. A settled loan is typically marked as "Settled" in your CIBIL report, which is viewed less favorably than a "Closed" status, indicating full repayment.

The impact of a loan settlement on your CIBIL score can be long-lasting, often remaining on your report for up to seven years. During this period, rebuilding your creditworthiness requires diligent efforts and responsible financial behavior. It's essential to adopt strategies that can help mitigate the negative effects and gradually improve your score.

Tip 1: Check Your CIBIL Report Regularly

One of the most effective ways to improve your CIBIL score is to monitor your credit report regularly. Checking your report helps you stay informed about your current credit status and spot any discrepancies or errors that could be negatively affecting your score. You can obtain a free copy of your CIBIL report once a year from CIBIL’s official website or through various financial service providers.

Regularly reviewing your CIBIL report allows you to track your progress and understand the factors influencing your score. It provides a detailed overview of your credit accounts, payment history, outstanding balances, and any public records such as loan settlements or bankruptcies. By keeping a close eye on these details, you can identify areas that need improvement and take corrective action promptly.

Benefits of Monitoring Your Credit Report

In addition to spotting errors, monitoring your CIBIL report helps you detect any signs of identity theft or fraudulent activity. If you notice unfamiliar accounts or transactions, you can take immediate steps to address the issue and protect your credit profile. Staying proactive and informed is crucial for maintaining and improving your CIBIL score.

Ensuring that your CIBIL report contains accurate information is vital for maintaining a healthy credit score. Inaccuracies or outdated information can unfairly drag down your score and hinder your efforts to rebuild it. Common errors include incorrect personal details, outdated account statuses, and incorrect payment histories.

To ensure accuracy, carefully review each section of your CIBIL report. Verify that your personal information, such as name, address, and contact details, is correct. Check that all your credit accounts are accurately listed, including the account numbers, credit limits, and outstanding balances. Pay particular attention to the payment history section, as any missed or late payments recorded in error can significantly impact your score.

What to Do If You Find Errors

If you identify any inaccuracies, promptly dispute them with CIBIL. You can submit a dispute online through the CIBIL website by providing the necessary documentation to support your claim. CIBIL will investigate the issue and make corrections if the error is validated. Ensuring your report is accurate not only improves your score but also enhances your credibility with potential lenders.

Tip 3: Pay Off Any Remaining Debts

Paying off any remaining debts is a crucial step in boosting your CIBIL score after a loan settlement. Outstanding debts, especially those with high balances or long overdue payments, continue to negatively affect your score. Clearing these debts demonstrates your commitment to financial responsibility and improves your creditworthiness.

Start by prioritizing your debts based on their interest rates and outstanding balances. Focus on paying off high-interest debts first, as they cost you more over time. You can use strategies like the debt snowball method, where you pay off smaller debts first to build momentum, or the debt avalanche method, where you tackle high-interest debts to save on interest payments.

Build Positive Payment History

Making timely and consistent payments on your remaining debts will gradually improve your CIBIL score. It shows lenders that you are capable of managing your financial obligations and reduces the overall amount of debt you carry. This positive payment behavior is recorded in your credit report and contributes to a healthier credit profile over time.

Tip 4: Rebuild Credit with Secured Credit Cards

Rebuilding your credit after a loan settlement can be challenging, but secured credit cards offer a viable solution. A secured credit card requires you to provide a security deposit, which acts as collateral and determines your credit limit. This reduces the risk for lenders and makes it easier for individuals with poor credit to obtain a card.

Using a secured credit card responsibly can significantly improve your CIBIL score. Make small, manageable purchases and ensure you pay off the balance in full each month. Timely payments are crucial, as they demonstrate your ability to manage credit responsibly.

Choose the Right Secured Card

It's important to choose a secured credit card from a reputable issuer that reports to the major credit bureaus, including CIBIL. This ensures that your responsible credit behavior is recorded and contributes to your credit improvement efforts. As your score improves, you may eventually qualify for unsecured credit cards, further enhancing your credit profile.

Tip 5: Maintain a Healthy Credit Utilization Ratio

The credit utilization ratio is the percentage of your available credit that you are currently using. It is a crucial factor in determining your CIBIL score, with a lower ratio indicating better credit management. Ideally, you should aim to keep your credit utilization ratio below 30% to positively impact your score.

To maintain a healthy credit utilization ratio, monitor your credit card balances and avoid maxing out your cards. If possible, spread your expenses across multiple cards to keep individual utilization rates low. Paying down existing balances can also help lower your overall utilization ratio and improve your score.

Increase Limits Carefully

Increasing your credit limit while keeping your spending consistent can further reduce your credit utilization ratio. However, be cautious with this approach, as it requires disciplined spending habits to avoid accumulating more debt. Maintaining a low credit utilization ratio demonstrates responsible credit behavior and contributes to a higher CIBIL score.

Tip 6: Diversify Your Credit Mix

A diverse credit mix, which includes a combination of credit types such as credit cards, personal loans, and home loans, can positively influence your CIBIL score. Lenders view a varied credit portfolio as a sign of good credit management and the ability to handle different types of credit responsibly.

If your credit profile lacks diversity, consider adding different types of credit accounts. For example, if you only have credit cards, you might explore taking a small personal loan or a secured loan. Ensure that you manage these accounts responsibly by making timely payments and keeping balances low.

Avoid Unnecessary Debt

Diversifying your credit mix not only improves your CIBIL score but also enhances your overall credit profile. It demonstrates to lenders that you can manage various forms of credit, making you a more attractive borrower. However, avoid taking on unnecessary debt solely to diversify your credit mix, as this can lead to financial strain and negatively impact your score.

Tip 7: Avoid New Hard Inquiries

Hard inquiries occur when a lender checks your credit report as part of the approval process for a loan or credit card. Each hard inquiry can slightly lower your CIBIL score and remains on your report for up to two years. Multiple hard inquiries within a short period can signal financial distress and negatively impact your score.

To avoid new hard inquiries, be selective about applying for new credit. Instead of applying for multiple credit cards or loans simultaneously, research and choose the best option that meets your needs.

Space Out Credit Applications

If you need to apply for credit, consider spacing out your applications over time. This allows your credit score to recover between inquiries and reduces the overall impact. Additionally, you can check if the lender offers a pre-approval process, which involves a soft inquiry that does not affect your score. Being mindful of hard inquiries helps protect your CIBIL score and supports your credit improvement efforts.

Improving your CIBIL score after a loan settlement requires dedication and a strategic approach. By understanding the factors influencing your score and implementing the tips outlined in this article, you can gradually rebuild your creditworthiness and regain financial confidence.

Regularly monitoring your CIBIL report, ensuring accurate information, and paying off remaining debts are foundational steps in this journey. Rebuilding credit with secured credit cards, maintaining a healthy credit utilization ratio, and diversifying your credit mix further contribute to a stronger credit profile. Avoiding new hard inquiries helps protect the progress you make.

While the path to a better CIBIL score may be challenging, consistent and responsible financial behavior will yield positive results over time. Stay committed to your credit improvement efforts, and you will eventually achieve a higher score, opening doors to better financial opportunities and a more secure future.