Loan Settlement kya hota hai? In simple words, it is a mutual agreement between a borrower and the bank where the borrower pays only a part of the outstanding loan amount, and the bank waives off the rest.

This usually happens when the borrower is unable to repay the loan due to financial difficulties, and the bank realizes that recovering the entire amount might not be possible. According to recent reports, nearly 10% of retail borrowers in India face repayment stress annually, making loan settlement a widely discussed solution.

In this blog, we will cover:

What loan settlement means

The detailed settlement process

Advantages and disadvantages

Impact on your credit score

Alternatives to loan settlement

Legal framework & FAQs

What is Loan Settlement?

Loan settlement is a financial arrangement where the borrower pays a negotiated lump sum to the lender, which is less than the full outstanding amount. The lender, in return, agrees to close the loan account and waive the remaining balance.

This is different from loan closure. In closure, the borrower repays the entire outstanding loan, which positively impacts credit history. In settlement, only a portion is paid, and the rest is written off, which negatively affects credit reports.

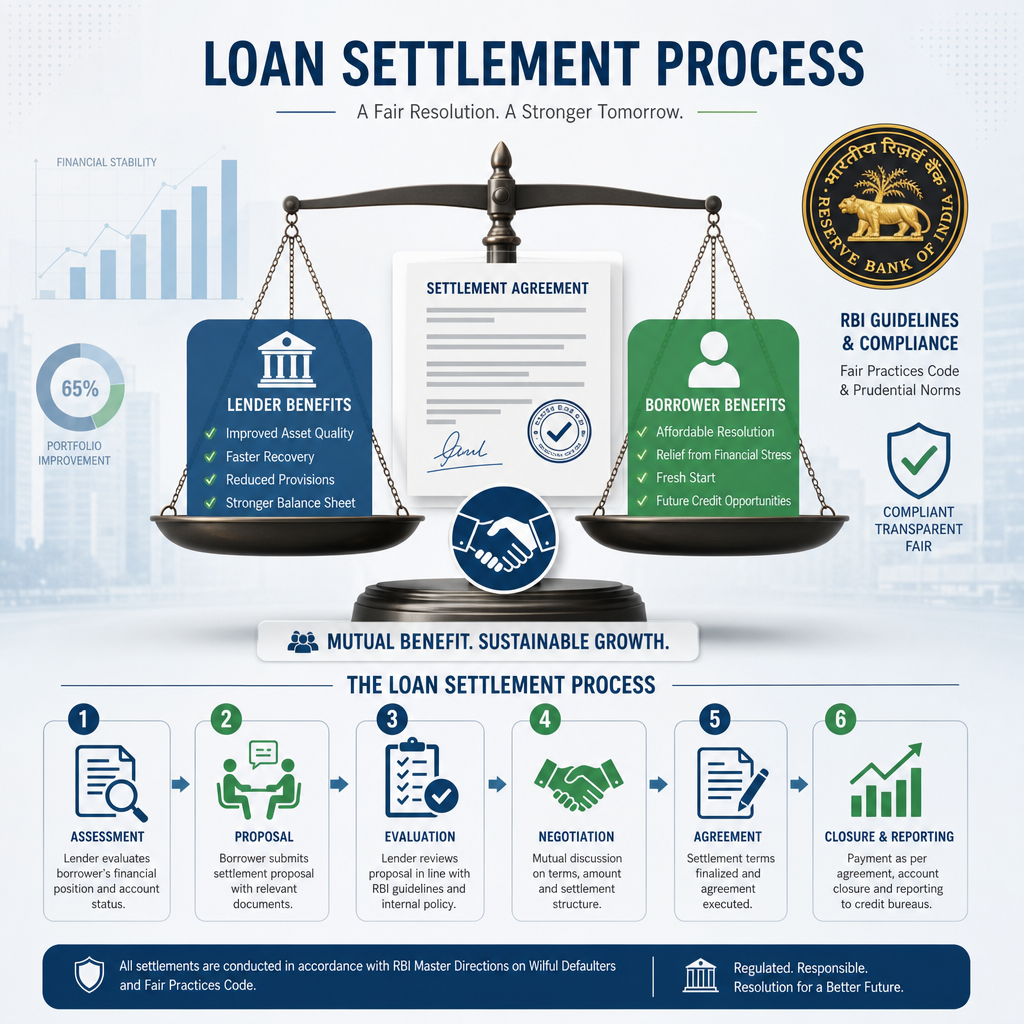

The Loan Settlement Process

1. Assessment of Financial Position

The borrower must assess how much they can afford to pay as a lump sum. Banks prefer upfront payments rather than stretched installments.

2. Approaching the Bank

Borrowers need to approach the bank with genuine reasons such as job loss, business failure, medical emergencies, or other financial hardships.

3. Negotiation and Proposal

Both parties negotiate on a settlement amount. Typically, banks may agree to 50–70% of the outstanding balance, depending on circumstances.

4. Settlement Agreement

The agreed amount and repayment deadline are put in writing. Borrowers must carefully review terms and keep copies of all communication.

5. Payment and Closure

The borrower pays the settled amount. The bank issues a No Dues Certificate (NOC) and settlement letter.

6. Reporting to Credit Bureaus

The account is reported as “Settled” in CIBIL and other credit bureaus. This stays on record for 7 years.

Advantages and Disadvantages

Advantages

Immediate Relief: Borrowers can reduce debt pressure.

Avoid Legal Action: Prevents SARFAESI Act action, Debt Recovery Tribunal (DRT) cases, or arbitration.

End Harassment: Stops frequent recovery calls and notices.

Bank Recovery: Banks recover at least part of the money instead of writing off the entire loan.

Disadvantages

Credit Score Damage: CIBIL score may drop by 75–150 points.

Negative Record: “Settled” status stays for up to 7 years.

Future Loans Impacted: Borrowers may face rejections or higher interest rates.

Lump Sum Requirement: Borrower needs immediate funds to pay settlement.

(Infographic Suggestion: Pros vs Cons Chart)

Case Study: Nashik NDCC OTS Scheme

The Nashik District Cooperative Bank (NDCC) launched a One Time Settlement (OTS) scheme in 2024. On the first day itself, 3 defaulters settled dues worth ₹21.3 lakh. This shows that banks prefer settlement when recovery through litigation may take years.

Such OTS schemes are commonly used by cooperative banks, NBFCs, and commercial lenders when faced with large volumes of stressed loans.

How Loan Settlement Impacts Your Credit Score

Loan settlement has serious consequences on your credit profile:

Credit score can drop by 75–150 points.

Account status marked as “Settled” instead of “Closed.”

The record remains visible to lenders for 7 years.

Borrowers may find it extremely difficult to get credit cards, car loans, or home loans in the future.

Ways to Rebuild Credit After Settlement:

Use secured credit cards against fixed deposits.

Pay EMIs and bills on time without default.

Keep credit utilization below 30%.

Monitor credit reports regularly and dispute errors.

Important Factors Before Choosing Loan Settlement

Evaluate Alternatives: Check restructuring, refinancing, or balance transfer options first.

Understand Legal Consequences: Settlement may prevent immediate litigation but impacts financial credibility.

Negotiate Properly: Ensure all agreements are written and signed by authorized bank officials.

Plan for Future Loans: Be prepared that getting loans in the next 5–7 years will be difficult.

Seek Expert Advice: A legal consultant can guide you to avoid unfair settlement terms.

Alternatives to Loan Settlement

Loan Restructuring: Extend tenure or reduce EMI.

Balance Transfer: Move the loan to another lender with lower interest.

Debt Consolidation: Merge multiple loans into one.

Asset Sale: Sell gold, property, or investments to repay.

Legal Assistance: Approach DRT or court if recovery agents use unlawful practices.

Legal and Regulatory Framework

RBI Guidelines: Banks are free to design their One Time Settlement (OTS) policies. There is no fixed universal rule.

SARFAESI Act, 2002: Banks can seize and sell secured assets for recovery. Settlement prevents escalation to this stage.

Debt Recovery Tribunal (DRT): Handles cases of loan defaults above ₹20 lakh.

Credit Information Companies Act, 2005: Mandates accurate reporting of settlement status to credit bureaus.

RBI Official Website on Banking Regulations)

Loan Settlement kya hota hai? It is a debt relief process where the borrower and bank agree on a partial repayment to close the account.

While it provides short-term relief and protects borrowers from legal harassment, it has long-term drawbacks like poor credit scores and restricted access to future loans.

👉 Our expert advice: Treat loan settlement as a last resort. Explore restructuring or repayment alternatives first. And if you do opt for settlement, ensure proper documentation and legal backing.

For professional assistance, AMA Legal Solutions provides expert legal services in loan settlement and financial disputes.

Facing financial stress? Considering a loan settlement? Don’t decide alone.

👉 Contact AMA Legal Solutions today for expert legal consultation and safeguard your financial future.