Getting stuck with unpaid loans chahe personal ho ya business can become a legal nightmare. But what happens when a borrower defaults? How do banks or NBFCs recover the money? This is where the loan recovery legal process in India kicks in. From sending legal notices to invoking the SARFAESI Act or opting for the arbitration route, financial institutions have multiple options at their disposal.

According to the Reserve Bank of India (RBI), as of March 2023, the gross non-performing assets (NPAs) of Indian banks stood at 3.9%. This makes loan recovery legal process a vital part of India’s financial ecosystem.

Let’s break it down step by step.

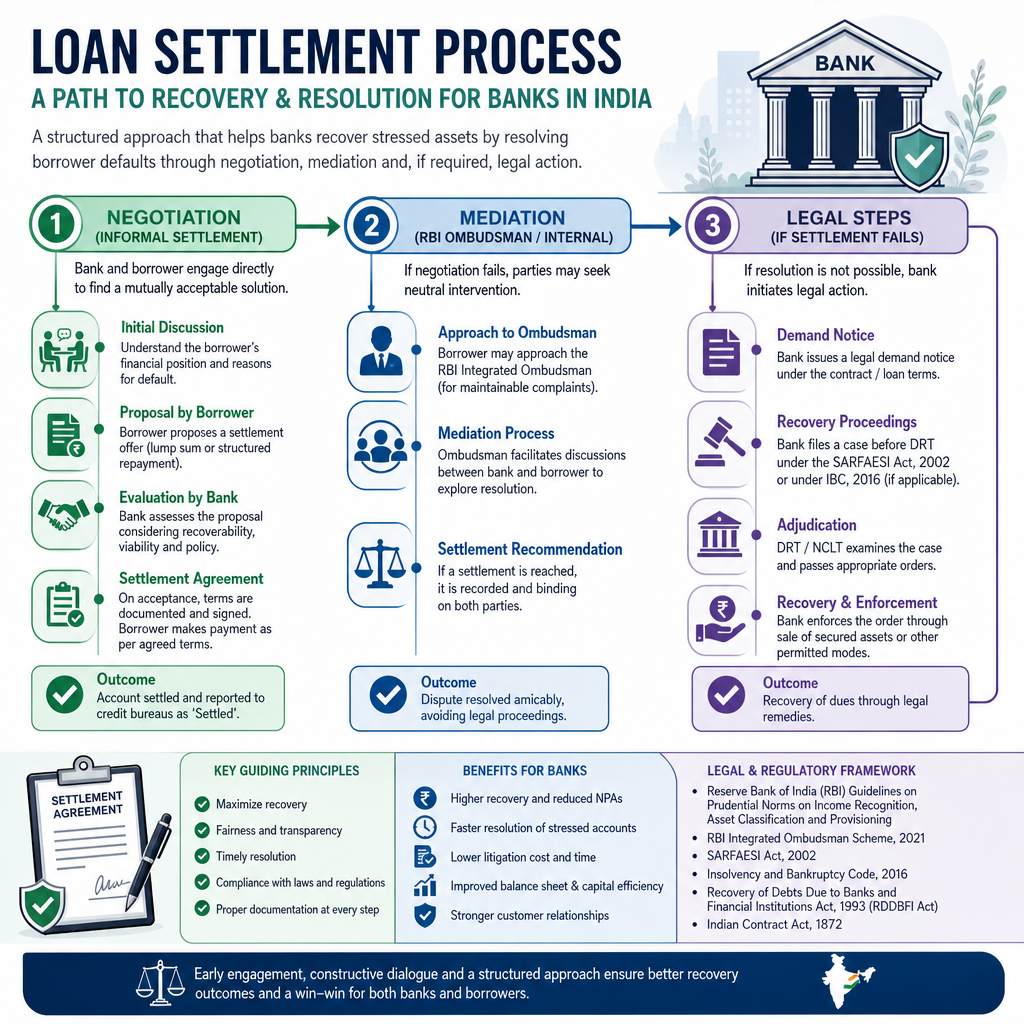

Understanding the Loan Recovery Legal Process

The loan recovery legal process refers to the structured legal framework through which lenders—primarily banks and NBFCs—seek to reclaim outstanding dues from defaulting borrowers.

Types of Loan Defaults:

Secured Loans: Loans backed by collateral (home loan, car loan)

Unsecured Loans: No collateral (credit card loans, personal loans)

Step-by-Step Legal Procedure for Loan Recovery in India

1. Reminder & Follow-up Notices

Banks usually initiate recovery by sending reminder calls, SMS, or emails. This is informal but part of the process.

2. Legal Notice to Borrower

If reminders fail, a formal legal notice is issued, demanding repayment within 15 to 30 days.

3. SARFAESI Act Action (For Secured Loans)

What is SARFAESI Act?

The SARFAESI Act (Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act), 2002 empowers secured creditors to enforce security interests without court intervention.

SARFAESI Process:

Notice under Section 13(2)

60 days for borrower to respond

If unpaid, Section 13(4) allows asset possession

Sale of assets through public auction

🔗 External Link: Read full SARFAESI Act on IndianKanoon

4. Debt Recovery Tribunal (DRT)

Banks can file an application before DRT if the default amount exceeds ₹20 lakhs.

DRT Powers:

5. Lok Adalat & Arbitration Route

Lok Adalat:

An alternative dispute resolution mechanism for small loans. Conducted under the Legal Services Authorities Act.

Arbitration:

For NBFCs or loans with arbitration clauses, this route is faster and less costly than traditional courts.

🔗 External Link: Arbitration in India – MCA

Borrower’s Legal Rights During Loan Recovery

Right to be heard

Right to fair valuation of assets

Right to challenge SARFAESI action before DRT

Right to receive notice before repossession

Precautions Lenders Must Take

Ensure documentation is in order

Maintain transparency with borrowers

Avoid coercion or illegal recovery agents

AMA Legal Tip: Loan recovery must adhere to RBI’s Fair Practices Code. Any violation is punishable under Indian law.

The loan recovery legal process in India is well-defined and legally structured to protect both lenders and borrowers. Whether through SARFAESI Act, DRT, or the arbitration route, recovery is only legal if due process is followed.

If you’re a borrower facing wrongful recovery actions, or a lender needing legal clarity, reach out to our expert team at AMA Legal Solutions today.

📊 According to RBI data, over ₹1.7 lakh crore was recovered through SARFAESI actions in FY2023 alone highlighting how critical this legal process is.

Need Legal Help with Loan Recovery?

📩 Contact AMA Legal Solutions – Gurugram’s Trusted Legal Partner for Loan Disputes and Debt Resolution.