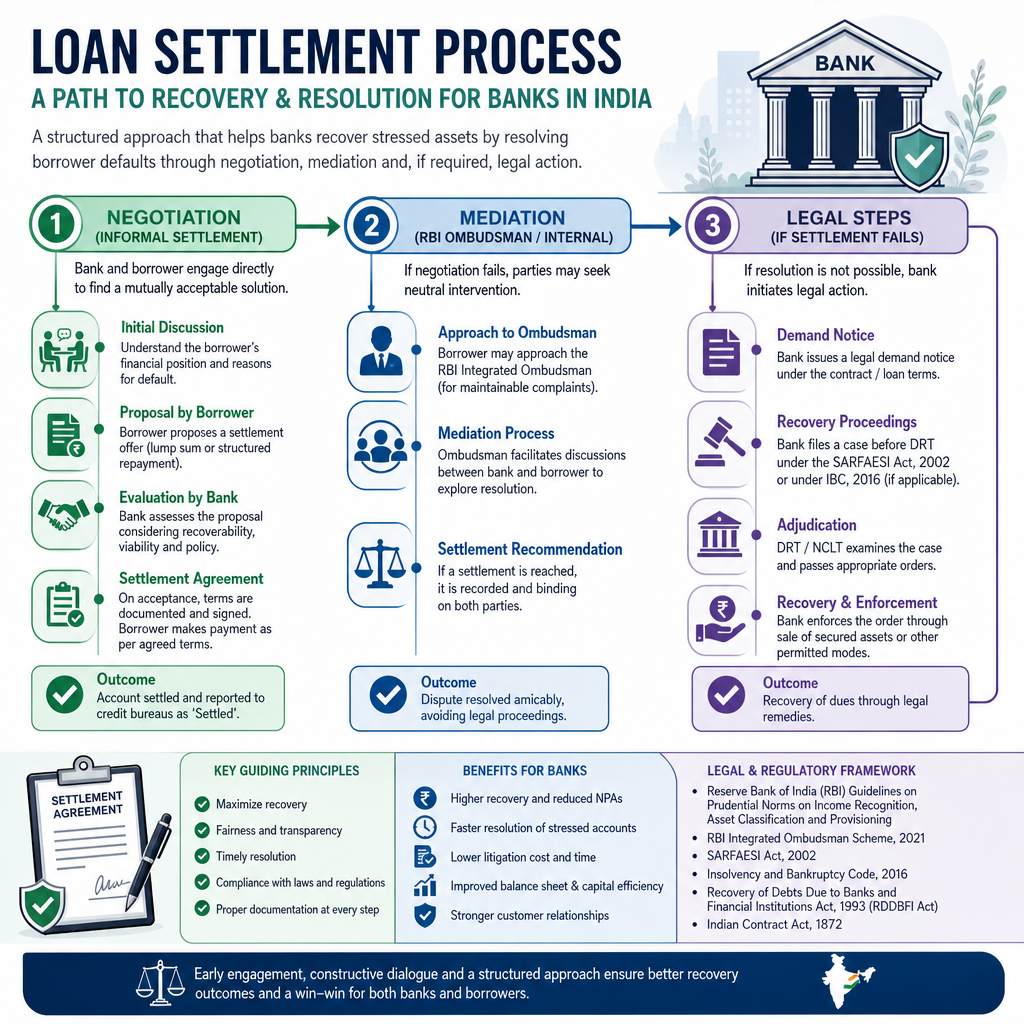

Unmanageable debt can make you feel entirely isolated, turning your daily routine into a stressful loop of avoiding unknown numbers and dreading collection notices. If an unexpected financial reversal has made it impossible to meet your monthly EMIs, understanding how financial institutions evaluate distressed accounts is your first step toward recovery. Achieving a top quality of loan settlement for banks means presenting a legally sound, realistic proposal that satisfies the lender's risk mitigation policies while permanently releasing you from your debt liabilities.

A personal loan settlement is a formal compromise where a lender agrees to accept a single, reduced lump-sum payment as full satisfaction of an outstanding debt, writing off the remaining balance. Securing a top quality of loan settlement for banks relies heavily on proving genuine financial hardship and demonstrating an absolute inability to pay the full amount over time. When structured properly by legal experts, this process ends all aggressive collection attempts, prevents prolonged litigation, and sets up a clear path to resolve your financial crisis.

Many borrowers in distress find themselves targets for aggressive third-party collection agencies. It is vital to recognize that your current default does not strip away your legal dignity or your statutory rights under Indian banking framework rules. By building a strategic defense rooted in Reserve Bank of India (RBI) mandates, you can navigate negotiations smoothly and work toward a clean break from your creditors.

The Operational Roadmap: How to Settle Personal Loan Default Issues

Resolving an outstanding liability requires a clear understanding of the standard Indian banking timeline. Lenders do not offer compromise terms immediately; they follow a rigid regulatory process before classifying an account as a bad asset and opening negotiations.

[Day 1-30: Overdue] ──> [Day 31-90: SMA 1 & 2 Status] ──> [Day 91+: NPA Classification] ──> [Month 6+: Settlement Window]

1. The Overdue Phase (Days 1 to 30)

The day an EMI is missed, the bank's automated systems flag the account. During this initial month, you will receive standard SMS warnings, email notifications, and automated telephonic reminders. Penal interest and late payment fees accumulate quickly during this time.

2. Special Mention Account (SMA) Risk Grading (Days 31 to 90)

To track systemic credit risks, the RBI requires banks to tag overdue accounts under specific risk buckets:

During the SMA-2 phase, banks routinely pass your file to external collection agencies to maximize pressure before the asset deteriorates further.

If an account stays past due for more than 90 days, it is officially classified as a Non-Performing Asset (NPA). Crossing this threshold forces the bank to stop booking regular interest on its ledger and begin provisioning for a potential bad debt write-off.

4. The Write-Off and Settlement Window (6 Months onwards)

Once an account has been an NPA for several months, the bank recognizes that recovering the full outstanding balance is unlikely. To clean up their balance sheets, lenders look for a compromise. This is where you can offer terms that match the top quality of loan settlement for banks—submitting a clear financial disclosure that encourages the credit committee to approve a major haircut rather than chasing a prolonged, expensive lawsuit.

Knowing Your Rights: RBI Guidelines on Fair Debt Recovery

You might be facing a temporary default, but you are fully protected by ironclad regulatory guardrails. The RBI has established clear, mandatory guidelines for financial institutions and their collection partners to prevent harassment and maintain professional boundaries.

Critical Legal Protection: Under the RBI's updated Fair Practices Code, lenders and their recovery agents are strictly prohibited from utilizing physical or mental intimidation, public humiliation, or verbal abuse against a borrower or their family members.

To safeguard yourself against aggressive collection strategies, keep these essential legal boundaries in mind:

Permissible Communication Hours: Recovery personnel can only contact or visit you between 8:00 AM and 7:00 PM. Any call, text message, or home visit outside of these hours is a direct violation of regulatory law.

Privacy Protections: Representatives cannot contact your neighbors, distant relatives, or workplace colleagues to expose your debt, unless those individuals are official co-borrowers or legal guarantors.

Verification Rule: Upon arriving at your home, an agent must immediately present a valid corporate ID card, a formal authorization letter from the lending bank, and a copy of the bank’s grievance redressal policy.

If an agency breaks these rules, you should file a formal complaint with the bank’s Principal Nodal Officer. If the issue isn't resolved within 30 days, you can escalate it directly to the RBI Banking Ombudsman. For severe infractions, our legal team specializing in banking and finance laws can step in, issue formal cease-and-desist notices, and help you take decisive action.

The Legal Realities of Bounced NACH Mandates and Checks

A major source of anxiety for borrowers is the sudden legal friction caused by a failed auto-debit. When your bank account lacks sufficient funds on your scheduled EMI date, your National Automated Clearing House (NACH) mandate or physical check bounces, creating serious legal responsibilities.

Section 138 of the Negotiable Instruments (NI) Act

If a physical check issued for debt repayment bounces due to insufficient funds, it triggers a criminal cause of action under Section 138 of the NI Act. The bank must serve you a formal legal notice within 30 days of the bounce, giving you a 15-day window to clear the specific balance. Failing to pay within this timeframe allows the lender to file a formal criminal complaint in a Magistrate court.

Section 25 of the Payment and Settlement Systems (PSS) Act

Because modern loan systems use digital auto-debits rather than paper checks, lenders rely heavily on Section 25 of the PSS Act.

Failed NACH Debit ──> Bank Issues 30-Day Legal Notice ──> 15-Day Cure Window ──> Criminal Complaint (Sec 25 PSS)

The provisions, penalties, and courtroom procedures of Section 25 of the PSS Act mirror Section 138 check-bouncing laws exactly. A digital mandate failure is treated as a criminal offense, carrying potential penalties of up to two years of imprisonment, a fine up to double the bounced amount, or both.

Banks often use these criminal filings as leverage to force an immediate payout. If you are served with a court summons, you need immediate legal drafting and defense support to build a strong counter-strategy. Resolving these matters requires proving operational discrepancies or a lack of legally enforceable liability, which is best handled through structured representation in civil and criminal litigation.

Strategic Comparison: Settlement vs. Restructuring

Deciding on the right path out of debt depends entirely on your current cash flow and long-term financial goals. Evaluating these options carefully will help you choose the best course of action.

Feature / Metric | One-Time Settlement (OTS) | Debt Restructuring |

Primary Approach | A single lump-sum payment closes the entire loan account permanently. | Modifying the original loan terms (extending tenure or lowering rates). |

Upfront Capital Need | Requires immediate access to funds (usually 20% to 50% of the total debt). | No large upfront payment needed; regular monthly payments resume. |

CIBIL Score Impact | Noticeable drop; account is reported as "Settled," making future credit tough to get. | Mild drop; account is marked as "Restructured" but stays active. |

Legal Status | All active civil and criminal recovery lawsuits are withdrawn after payment. | The original contract stays active; new defaults can trigger new lawsuits. |

Best Suited For | Borrowers with access to family funds, an inheritance, or asset sales. | Borrowers facing temporary income cuts who expect their cash flow to recover. |

Decoding the CIBIL Impact: "Settled" vs. "Closed" Status

While a settlement resolves immediate legal pressure, it leaves a long-term mark on your financial history. Understanding how credit bureaus treat this step is crucial for rebuilding your finances later.

Once your settlement is completed, the bank reports the final update to credit bureaus like TransUnion CIBIL. The account status is then changed to "Settled."

[Account Status: Settled] ──> High-Risk Flag for Lenders ──> Future Credit Requests Denied

This is completely different from a "Closed" status, which shows that a loan was paid back in full according to the original agreement. A "Settled" status tells future lenders that you were unable to pay back the full amount, resulting in a loss for the bank. This can lower your credit score by 50 to 100 points, making it hard to secure unsecured loans or credit cards for five to seven years.

Rebuilding Your Credit Post-Settlement

If a settlement is your only realistic choice, you can systematically repair your credit profile over time:

Get a Secured Credit Card: Put money into a fixed deposit (FD) and get a credit card backed by that deposit. Use it for small, daily purchases and pay the bill in full every month.

Utilize an Overdraft Limit: Managing a small overdraft account backed by an FD builds a steady history of reliable, on-time repayments.

Monitor Your Credit Report: Make sure your lender updates your outstanding balance to zero once the settlement is finalized. If any errors show up, open an official dispute on the CIBIL portal using your No Dues Certificate.

Comprehensive FAQs on Indian Loan Settlements

What factors establish a top quality of loan settlement for banks?

A top quality of loan settlement for banks involves providing clear proof of severe financial hardship, offering a realistic lump-sum payment, and maintaining complete transparency. Lenders prefer structured proposals that allow them to recover cash quickly without entering a lengthy legal battle.

Can a bank reject my offer for a personal loan settlement?

Yes, banks are not legally required to accept a settlement proposal. If their internal checks show you have hidden assets, alternative income sources, or the clear financial capacity to pay your full debt, they may reject your offer and pursue asset recovery instead.

Is imprisonment a possibility for defaulting on a personal loan in India?

A simple failure to repay an unsecured personal loan is a civil matter and will not result in jail time. However, if an auto-debit or check bounces and you ignore the resulting court summons under Section 138 of the NI Act or Section 25 of the PSS Act, a magistrate can issue warrants for non-appearance.

How does the top quality of loan settlement for banks benefit a distressed borrower?

Aiming for a top quality of loan settlement for banks ensures that the lender waives maximum penal charges, cuts down the core principal balance, and provides an official No Dues Certificate. This brings an end to all collection activities and stops future legal claims.

What is a No Dues Certificate, and why do I need it?

A No Dues Certificate (NDC) is an official document from your bank confirming that your settlement payment was received and the account is closed with no further liability. This certificate protects you against future collection actions and is required to update your credit history.

Can personal loan defaults be resolved through a Lok Adalat?

Yes, banks frequently refer long-term NPA accounts to Lok Adalats to find a quick compromise. Settlements reached in these forums are legally binding and carry the full weight of a civil court decree, offering an efficient way to resolve disputes.

Can recovery agents call me at any time of day?

No, RBI guidelines state that recovery agents can only call or visit your home between 8:00 AM and 7:00 PM. Any communication outside of this window violates the RBI's Fair Practices Code and should be reported to the bank's grievance cell.

How long does a "Settled" status stay on a CIBIL report?

A "Settled" remark stays on your credit history for seven years. While it will impact your credit access during this time, you can gradually minimize its effect by maintaining excellent payment histories on new, secured lines of credit.

Secure Your Financial Future and Regain Peace of Mind

Dealing with deep financial distress and collection pressure can be an exhausting experience. However, Indian banking regulations provide clear, lawful pathways for borrowers to resolve unmanageable debt and start fresh. By focusing on a well-structured proposal that meets the standard criteria for a top quality of loan settlement for banks, you can protect yourself from litigation and close your open defaults permanently.

Succeeding in these negotiations requires a strong understanding of banking laws, proper documentation, and steady professional boundaries. Attempting to manage bank recovery teams on your own often leads to unfavorable terms that fail to provide complete legal protection.

If you are ready to stop collection pressure and settle your outstanding debts through proper legal channels, contact our specialized Loan Settlement Practice Desk at AMA Legal Solutions today. Our attorneys will evaluate your loan accounts, design a tailored legal strategy, manage all communications with your creditors, and protect your rights. Schedule a consultation through our civil legal remedies portal or contact our offices to review your case with a dedicated attorney. Reach out to our team via our comprehensive personal loan settlement services desk to establish control over your financial recovery today.

Our Full-Service Practice Areas