Your credit score plays a decisive role in shaping your financial future. Whether you’re applying for a personal loan, a home loan, or a new credit card, lenders rely heavily on your TransUnion CIBIL score to judge your creditworthiness.

TransUnion CIBIL, India’s foremost credit bureau, tracks your repayment patterns, loan history, and credit card behavior to assign you a score that determines how easily you can access credit.

But what happens if your score drops due to missed payments or loan settlements? Can you legally and practically rebuild it?

This comprehensive guide from AMA Legal Solutions - Gurugram’s trusted law firm for loan settlement and debt resolution — explains everything about TransUnion CIBIL, its operations, and the most effective ways to increase your CIBIL score using both financial discipline and legal expertise.

What is TransUnion CIBIL?

TransUnion CIBIL (Credit Information Bureau India Limited) is India’s first and most trusted credit information company, licensed by the Reserve Bank of India (RBI). It collects and maintains credit data for millions of individuals and businesses across India, generating CIBIL Reports and CIBIL Scores that reflect one’s financial reliability.

Key Facts about TransUnion CIBIL

Established in 2000, headquartered in Mumbai

Acquired by TransUnion, a global analytics company, in 2016

Tracks repayment behavior of 600+ million individuals and 32 million businesses

CIBIL Score ranges from 300 to 900

Higher scores (750+) signify excellent creditworthiness

Banks, NBFCs, and credit institutions report customer data to CIBIL, which compiles it into your credit profile and calculates your score accordingly.

How Does TransUnion CIBIL Work?

Whenever you borrow or use a credit card, your lender submits details of your repayment behavior to CIBIL. The bureau compiles this data to prepare a comprehensive CIBIL report that includes:

CIBIL Score Calculation Process

Data Collection – Lenders share monthly repayment data.

Evaluation – CIBIL analyzes repayment regularity and credit usage.

Scoring – You’re assigned a score between 300 and 900.

Distribution – Banks view your score when you apply for new credit.

Understanding Your CIBIL Score

Your CIBIL score is a 3-digit number representing your credit health. It’s a snapshot of your repayment history and debt management skills.

Score Range | Category | Loan Approval Chances |

|---|

750 – 900 | Excellent | Very High |

700 – 749 | Good | High |

650 – 699 | Fair | Moderate |

550 – 649 | Poor | Low |

300 – 549 | Very Poor | Very Low |

A score above 750 improves your chances of loan approval, while scores below 650 may lead to rejections or higher interest rates.

Factors Affecting Your CIBIL Score

TransUnion CIBIL evaluates multiple parameters to compute your score.

1. Repayment History

Your payment track record is the most crucial factor.

2. Credit Utilization Ratio

Using more than 30–40% of your total credit limit signals financial stress.

3. Number of Hard Inquiries

Applying for multiple loans or cards within a short span lowers your score.

4. Credit Mix

Maintaining a combination of secured (home loan) and unsecured (credit card) credit boosts your credibility.

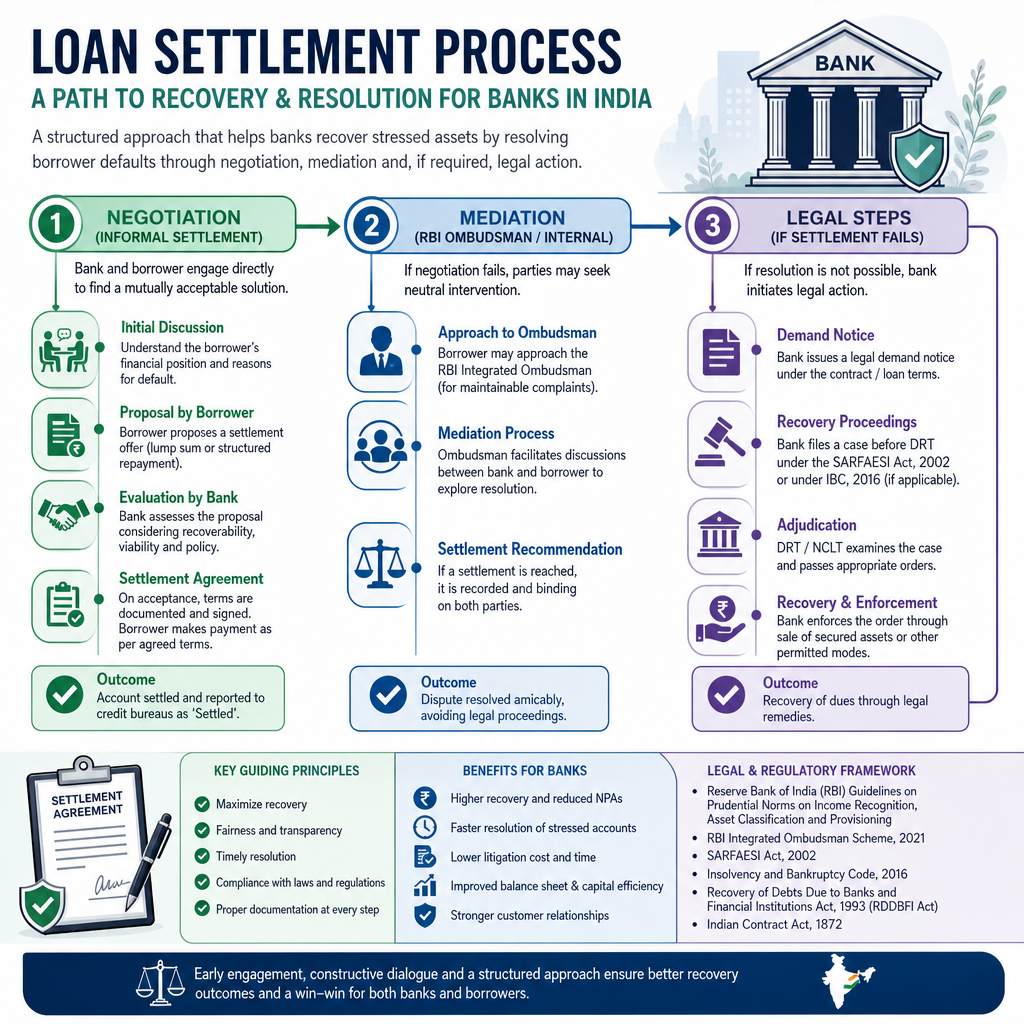

Loan settlements or “write-offs” show partial payments and are viewed negatively by lenders.

How to Increase Your CIBIL Score – Step-by-Step Guide

Improving your CIBIL score isn’t instant - it’s a steady process involving consistent payments, reduced debt, and sometimes, legal guidance. Follow this step-by-step approach:

Step 1 – Get Your Latest CIBIL Report

Visit TransUnion CIBIL’s official site.

Download your free annual credit report.

Review all entries for errors or outdated data.

Step 2 – Identify and Dispute Errors

If a loan you’ve closed still appears “open” or “settled,” file a dispute online through the CIBIL portal.

The lender and CIBIL typically resolve such disputes within 30 days.

Step 3 – Clear Outstanding Balances

Pay off overdue EMIs and credit card dues completely, not partially.

Partial payments still mark your account as “settled.”

Step 4 – Reduce Credit Utilization

Keep usage below 30% of your credit limit.

If needed, request a limit enhancement to improve your ratio.

Step 5 – Avoid Multiple Loan Applications

Step 6 – Maintain a Balanced Credit Mix

Step 7 – Seek Legal Help for Loan Settlements

If your CIBIL score dropped after a loan settlement, legal support from AMA Legal Solutions can help you:

Negotiate lawful settlements with lenders

Rectify “settled” remarks to “closed” status

Submit formal representations to CIBIL and banks

Legal Support by AMA Legal Solutions

At AMA Legal Solutions, we specialize in handling complex credit issues through transparent legal processes.

We help clients legally settle their debts with banks and NBFCs to ensure proper loan closure and minimal CIBIL impact.

2. CIBIL Correction & Representation

Our experts submit correction requests to TransUnion CIBIL and lenders to remove or amend negative remarks.

If you’re facing harassment from recovery agents, we take immediate legal action under RBI and Consumer Protection Laws.

4. Financial Rehabilitation

We create customized financial and legal strategies to rebuild your score and regain your financial independence.

Common Myths About CIBIL Scores

Myth | Reality |

|---|

Checking my score lowers it | False – Self-checks are soft inquiries |

Settling a loan improves score | False – Settlements reduce it |

Credit cards hurt your score | False – Proper usage helps build credit |

CIBIL score can’t be improved | False – With legal and financial discipline, it can |

Case Study: From Low Score to Financial Freedom

Client: R.K., an entrepreneur from Delhi

Issue: Low CIBIL score (520) due to multiple defaults during COVID-19

Action:

Legal representation by AMA Legal Solutions for debt negotiation

“Settled” status converted to “Closed”

Strategic financial guidance for 9 months

Result: Score improved from 520 → 740 in under a year.

Your TransUnion CIBIL score is the gateway to your financial future. A low score can make loans expensive or unattainable — but with the right mix of discipline and legal support, you can rebuild your credibility and unlock better financial opportunities.

At AMA Legal Solutions, we don’t just fix scores - we protect your legal rights and guide you through lawful, ethical, and effective methods to restore your credit profile.

💼 Contact AMA Legal Solutions today to start improving your CIBIL score and take control of your financial journey.