Over the last decade, Non-Banking Financial Companies (NBFCs) have become one of the fastest-growing lenders in India. From personal loans and business loans to vehicle finance, NBFCs provide quick credit to millions of borrowers who may not always qualify for bank loans. However, when repayment becomes difficult due to financial stress, borrowers often look for a solution through loan settlement for NBFC loan.

Unlike banks, NBFCs have more flexible lending structures, but this also means their recovery process can sometimes feel overwhelming for borrowers. In such situations, a professional NBFC loan settlement in Delhi can help reduce financial stress, prevent legal complications, and negotiate a fair resolution.

At AMA Legal Solutions, we specialize in helping individuals and businesses settle their NBFC loans legally and efficiently. This comprehensive guide will walk you through the entire process of NBFC loan settlement—its legal framework, benefits, risks, and practical strategies to achieve a stress-free financial resolution.

What is Loan Settlement for NBFC Loan?

Loan settlement for NBFC loan refers to a negotiated agreement between the borrower and the NBFC, where the borrower pays a reduced amount compared to the total outstanding balance, and the NBFC agrees to treat it as full and final payment.

Key Highlights:

Applicable to personal loans, business loans, gold loans, and vehicle loans issued by NBFCs.

Can be negotiated when repayment is impossible due to genuine financial hardship.

Helps avoid prolonged litigation and harassment from recovery agents.

Must be done legally to avoid future disputes.

Borrowers in metro cities like Delhi often consult legal experts for NBFC loan settlement in Delhi to ensure compliance with the law.

When Should You Consider NBFC Loan Settlement?

Settling an NBFC loan is not always the first option it should be considered under genuine circumstances. Some situations where settlement may be the right choice include:

Severe Financial Hardship

High Interest Burden

Multiple Loan Defaults

Legal Action Threats

👉 To know your eligibility, consult our loan settlement experts for personalized guidance.

Legal Framework Governing NBFC Loan Settlement in India

Unlike banks, NBFCs operate under the Reserve Bank of India (RBI) regulatory framework but do not fall under the Banking Regulation Act, 1949. Here’s what you need to know:

RBI Guidelines for NBFCs

NBFCs are required to follow fair recovery practices.

They can use arbitration or civil suits to recover loans.

Settlement is a legally valid alternative, provided both parties agree.

For professional handling of arbitration and settlement cases, visit AMA Legal Solutions Loan Settlement Services.

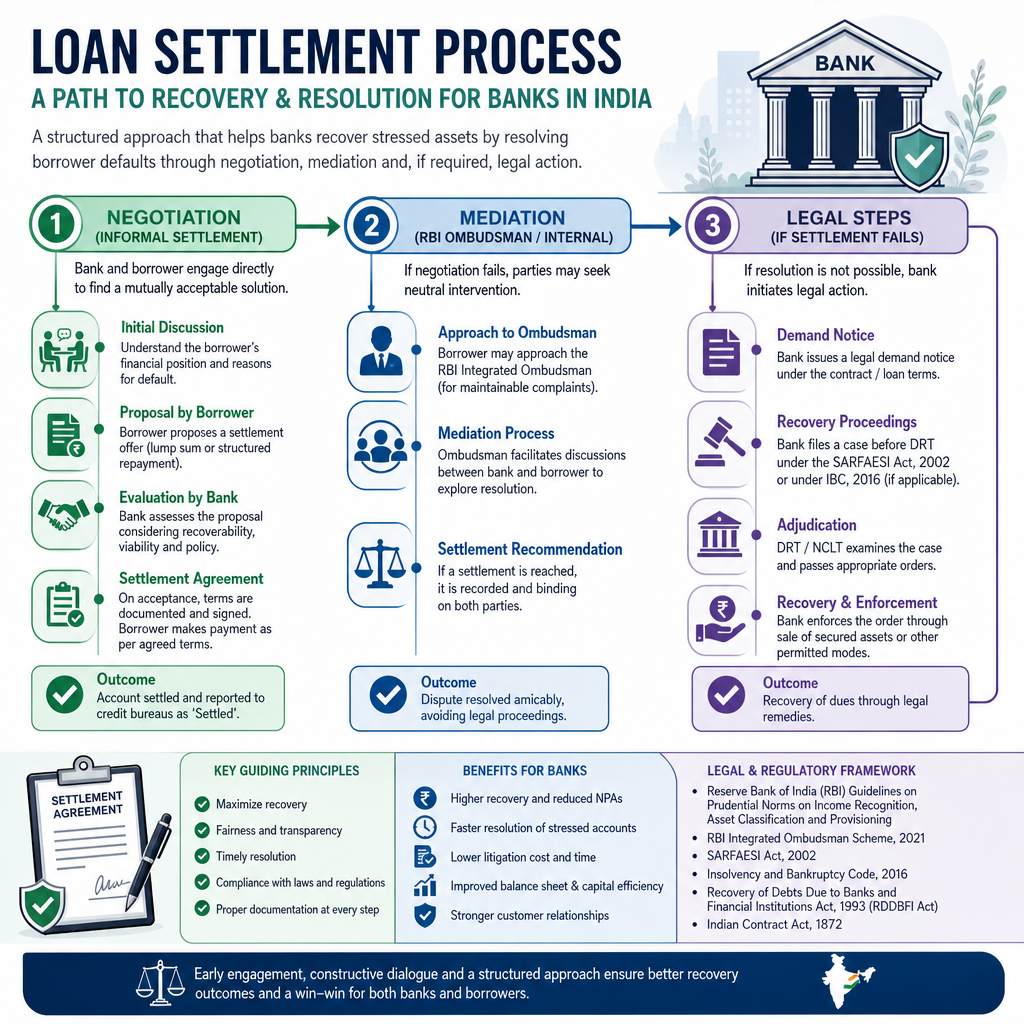

Step-by-Step Process of Loan Settlement for NBFC Loan

Here’s a structured approach to NBFC loan settlement:

Step 1: Assess Your Financial Position

Calculate total outstanding, overdue interest, and penalties.

Identify the maximum lump sum you can pay for settlement.

Step 2: Hire Legal Experts

Step 3: Negotiate Settlement Terms

Propose a one-time settlement amount.

Ensure the settlement covers principal, partial interest, and waiver of penalties.

Step 4: Draft a Settlement Agreement

Step 5: Obtain NOC & Close the Loan

Benefits of Loan Settlement for NBFC Loan

Reduced Financial Burden – Pay less than the total outstanding.

Avoid Harassment – Prevents aggressive recovery practices.

Legal Protection – Ensures the NBFC cannot pursue further claims.

Peace of Mind – Close the loan and focus on financial recovery.

Risks & Challenges in NBFC Loan Settlement

While settlement has clear benefits, borrowers should be aware of potential challenges:

Credit Score Impact – "Settled" status may affect future loan eligibility.

Tax Liability – Waived amounts may be considered taxable income.

NBFC Rejection – NBFCs may refuse settlement if the offer is too low.

Fraud Risks – Unverified agents may exploit borrowers; always deal through legal professionals.

How AMA Legal Solutions Assists with NBFC Loan Settlement

At AMA Legal Solutions, we offer end-to-end assistance for NBFC loan settlement in Delhi and across India:

Legal Consultation – Reviewing your loan agreements and financial position.

Negotiation with NBFCs – Direct discussions with lenders for the best settlement.

Arbitration Support – Handling ongoing arbitration or recovery cases.

Drafting Agreements – Ensuring legally binding settlement terms.

Post-Settlement Support – Assisting with NOC collection and credit repair advice.

Our team ensures a transparent, ethical, and stress-free loan settlement process.

Loan Settlement vs. Loan Restructuring for NBFC Loans

Criteria | Loan Settlement | Loan Restructuring |

|---|

Objective | Close loan at reduced amount | Modify repayment terms |

Credit Impact | Moderate | Lower impact |

Timeline | Quick | Extended |

Legal Agreement | Required | Required |

👉 To know which option suits you best, consult our legal advisors.

Practical Tips for Successful NBFC Loan Settlement

Document All Communication – Keep written proof of settlement terms.

Offer Realistic Amounts – Avoid very low offers that NBFCs may reject.

Avoid Unauthorized Agents – Work only with registered legal firms like AMA Legal Solutions.

Check Your Credit Report – After settlement, verify updated loan status.

Settling an NBFC loan is not just about reducing debt it’s about protecting your legal rights and securing your financial future. With rising NBFC lending in India, disputes and defaults are common. By opting for a professional loan settlement for NBFC loan, you can avoid harassment, reduce liabilities, and achieve peace of mind.

At AMA Legal Solutions, we provide expert guidance for NBFC loan settlement in Delhi, ensuring every step is legally compliant and in your best interest. If you are struggling with NBFC loans, don’t wait for matters to escalate reach out today and secure your financial freedom.